Here’s something really positive about the US economy

It’s hard to get away from the negative headlines that have accompanied the Silicon Valley Bank crisis. Recession calls have seen a renewed uptick since the crisis unfolded, whereas they were dying down prior to that, thanks to positive economic data in February and early March. Note that what little real-time data we’ve seen since then isn’t pointing to a sudden stop for the economy. Of course, we’ll continue to track the data, but at this point, we continue to believe that the economy can avoid a recession this year.

The biggest positive that the economy currently has going for it right now is employment. Payroll growth has averaged just over 350,000 over the past three months, and the unemployment rate is at 3.6%, close to 50-year lows. Weekly initial claims for unemployment benefits remain low, suggesting that employment growth continues to run strong even in March.

Nevertheless, even when discussions of the labor market arise, Tech sector layoff announcements loom disproportionately large. We wrote about this over a month ago, putting these layoffs in perspective. The companies making these announcements saw payrolls surge after the pandemic, and now they’re retrenching.

In any case, there’s something else that you don’t hear a lot about amid all the negative headlines.

A potentially bigger story

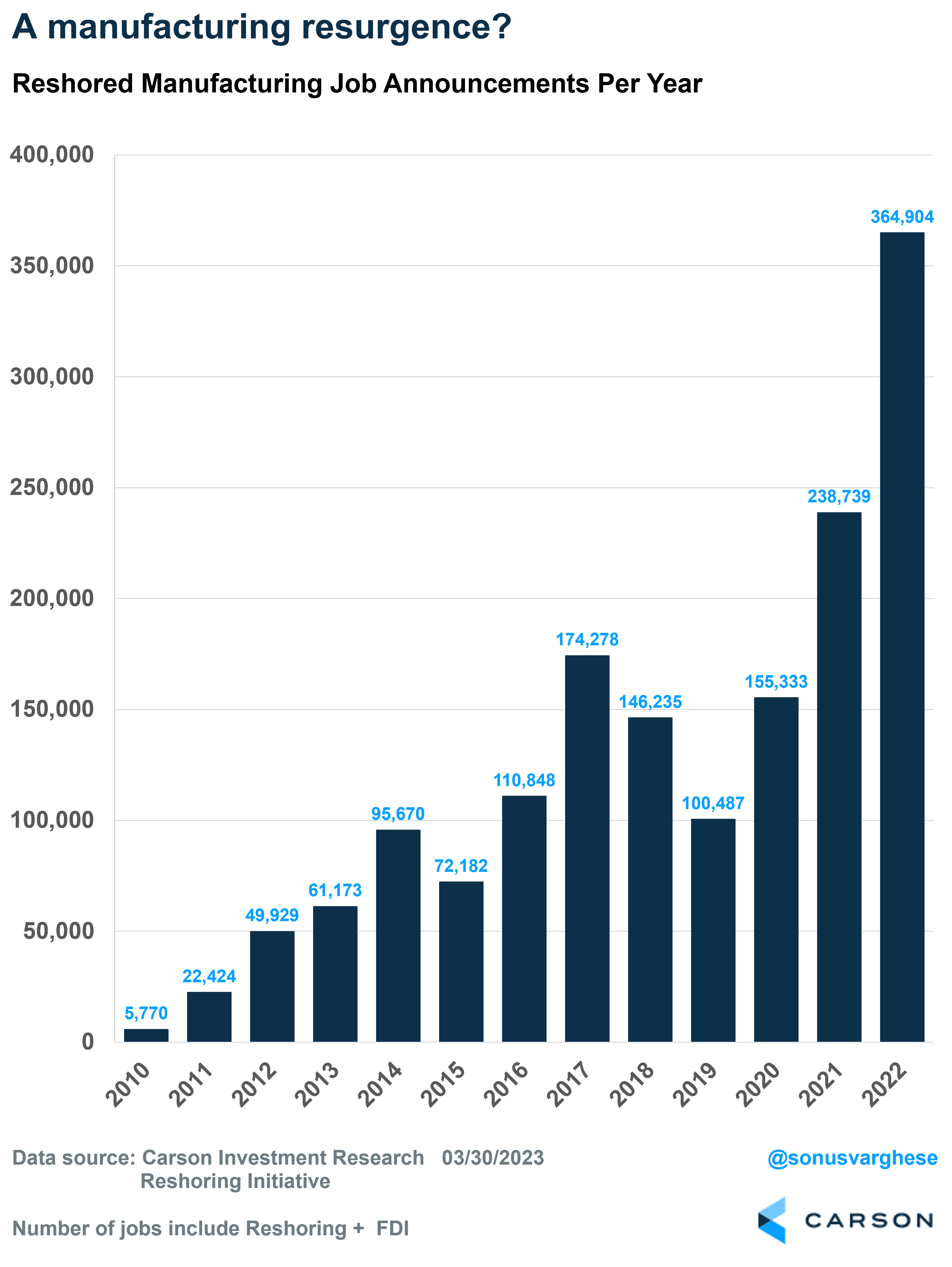

As good as the labor market is right now, what’s interesting is that American companies reshored a record 365,000 manufacturing jobs in 2022. These numbers, reported by the Reshoring Initiative, include jobs that had previously been done in other countries and jobs created by foreign-owned companies here in the US.

The 2022 number is a 53% increase from 2021, which itself saw a 54% increase from 2020. These numbers are typically volatile, but the sheer magnitude of the increase over the last few years suggest we have the making of a trend.

The report points out that the increase was driven by a surge in electric vehicle batteries and chips, along with a continued uptrend in industries like electrical equipment, chemicals, transportation equipment, and medical equipment.

The increase from 2020-2022 was partly due to companies recognizing that supply chains extending across the world are vulnerable to disruptions and geopolitical events.

The other big reason is that manufacturing investment in the US is surging after Congress and the President passed last year’s “Inflation Reduction Act” (IRA) and the “Chips and Science Act.” We wrote at the time that the IRA was poorly labeled, but it was a big deal, including:

- Taking a practical, all of the above approach, to the energy transition, with money for clean energy but also nuclear power and the oil and gas industry.

- Tax credits and subsidies for clean energy companies, with even traditional infrastructure companies (like midstream pipelines) benefiting.

- Provisions designed to revive US manufacturing and counter China, with the US engaging in industrial policy on a scale we haven’t seen in recent decades.

We wrote at the time that this could potentially incentivize investment in technology and increase productivity, which would be good for all workers, let alone economic growth and corporate profits.

It’s nice to see that it’s happening on the ground. Electric vehicle batteries were the most active product to be reshored in 2022!

And there’s even more evidence.

Manufacturing construction is booming

The construction industry has clearly taken a hit from the Federal Reserve’s aggressive interest rate hikes. Mortgage rates surged as a result, and that froze home-buying activity. Single-family housing starts collapsed 32% year-over-year in February 2023. Multi-family housing is holding on, but that’s because a lot of units remain under construction, and rental demand is high thanks to low housing inventory.

And now, with the bank crisis, commercial real estate has come under the microscope. Small banks make a lot of loans to this sector, and a pullback in lending will hurt. Though commercial and office construction had already been slowing before the crisis. You just have to walk across the downtown of any major metro in America to realize that offices are not in great demand.

Yet, here’s what’s interesting and important:

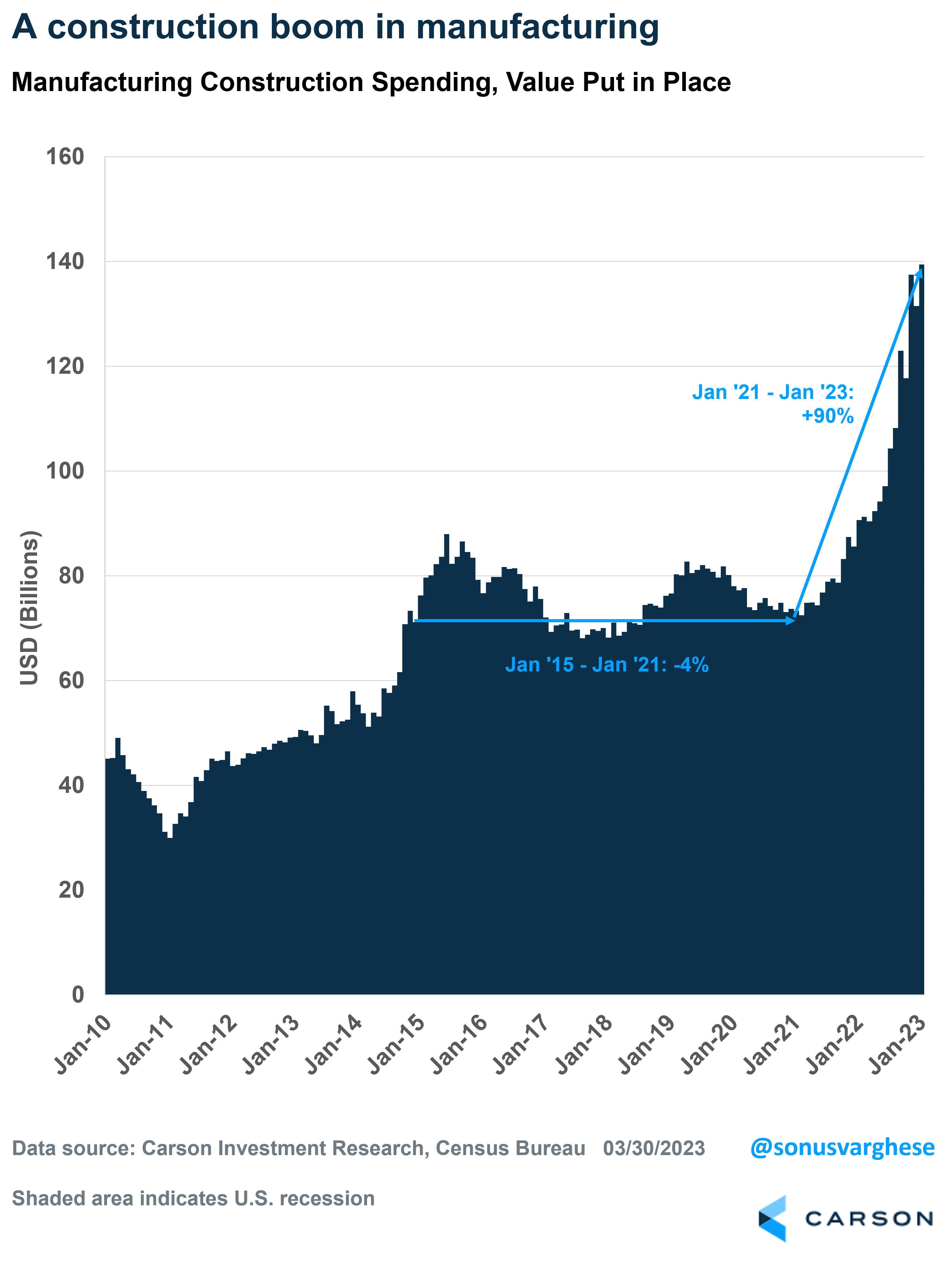

The total dollar value of all private construction spending rose about $61 billion over the year through January, representing a 4.4% y/y increase. Of this, almost $49 billion came from manufacturing construction spending.

As of January, manufacturing construction spending in dollar terms is up 54% y/y and it is up 90% from 2 years ago.

A year ago (Jan ’22) manufacturing construction made up just about 6.5% of total private construction in the US. It’s risen to almost 10% now (Jan ’23).

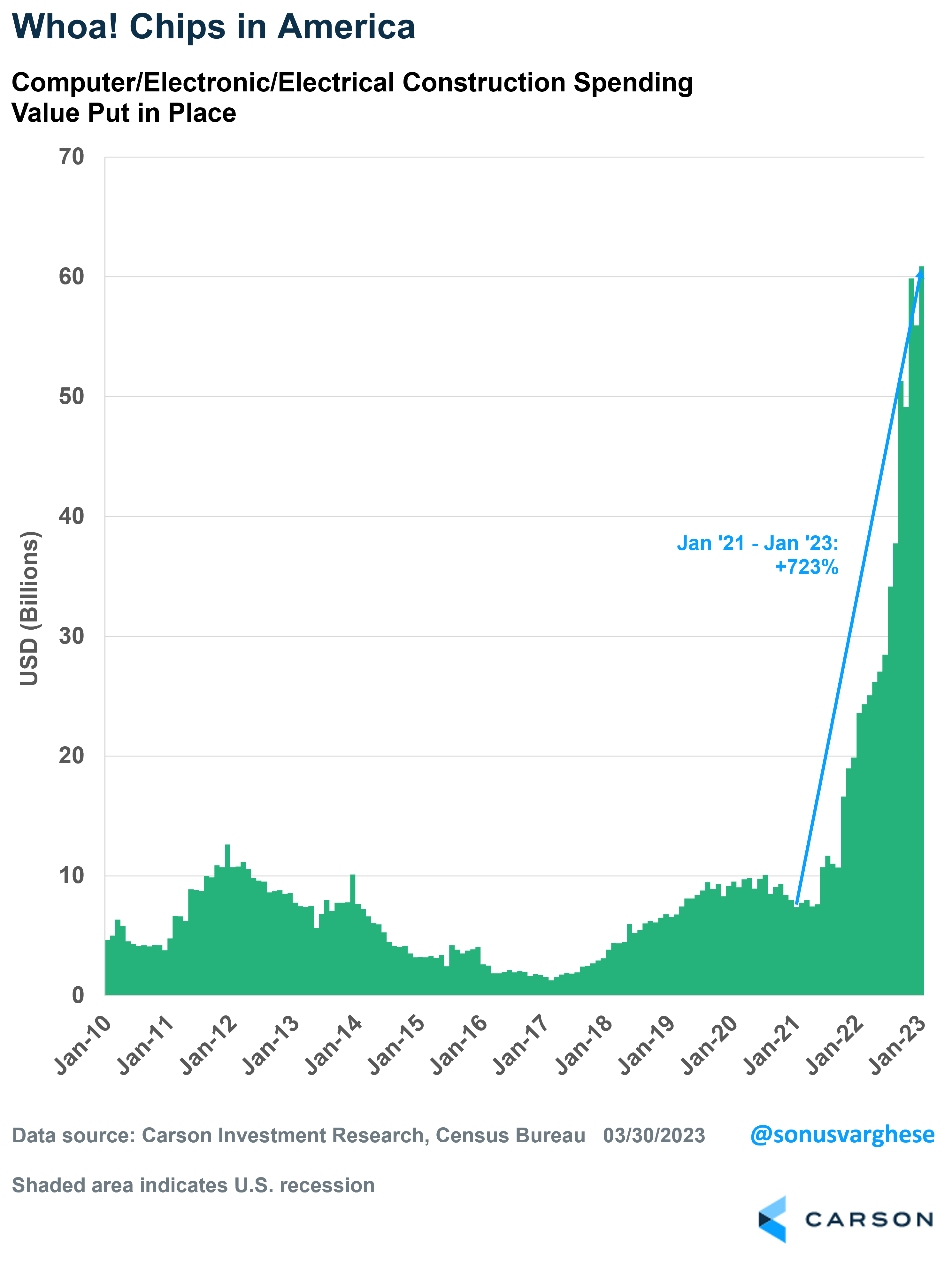

And this is almost entirely being driven by the computers and electronics industry, including investment in semiconductor plants, where construction spending is up 158% y/y and a whopping 723% over the last 2 years!

Construction spending across the rest of the manufacturing industry is up 17% y/y – not too shabby by itself, but pales in comparison to what’s happening on the computers and electronics side.

Of course, a lot of this is driven by subsidies and tax credits, and that’s not going to continue year after year.

But investment spending tends to feed on itself, especially since that can boost productivity. That’s potentially a huge positive for the American economy over the next decade.

Sometimes it helps to pull back and look at the bigger, and longer-term, economic picture.

The Carson Investment Research newsletter offers up-to-date market news, analysis and insights. Subscribe today! "*" indicates required fields![]()

Stay on Top of Market Trends