The October payroll report was weaker than expected on several fronts:

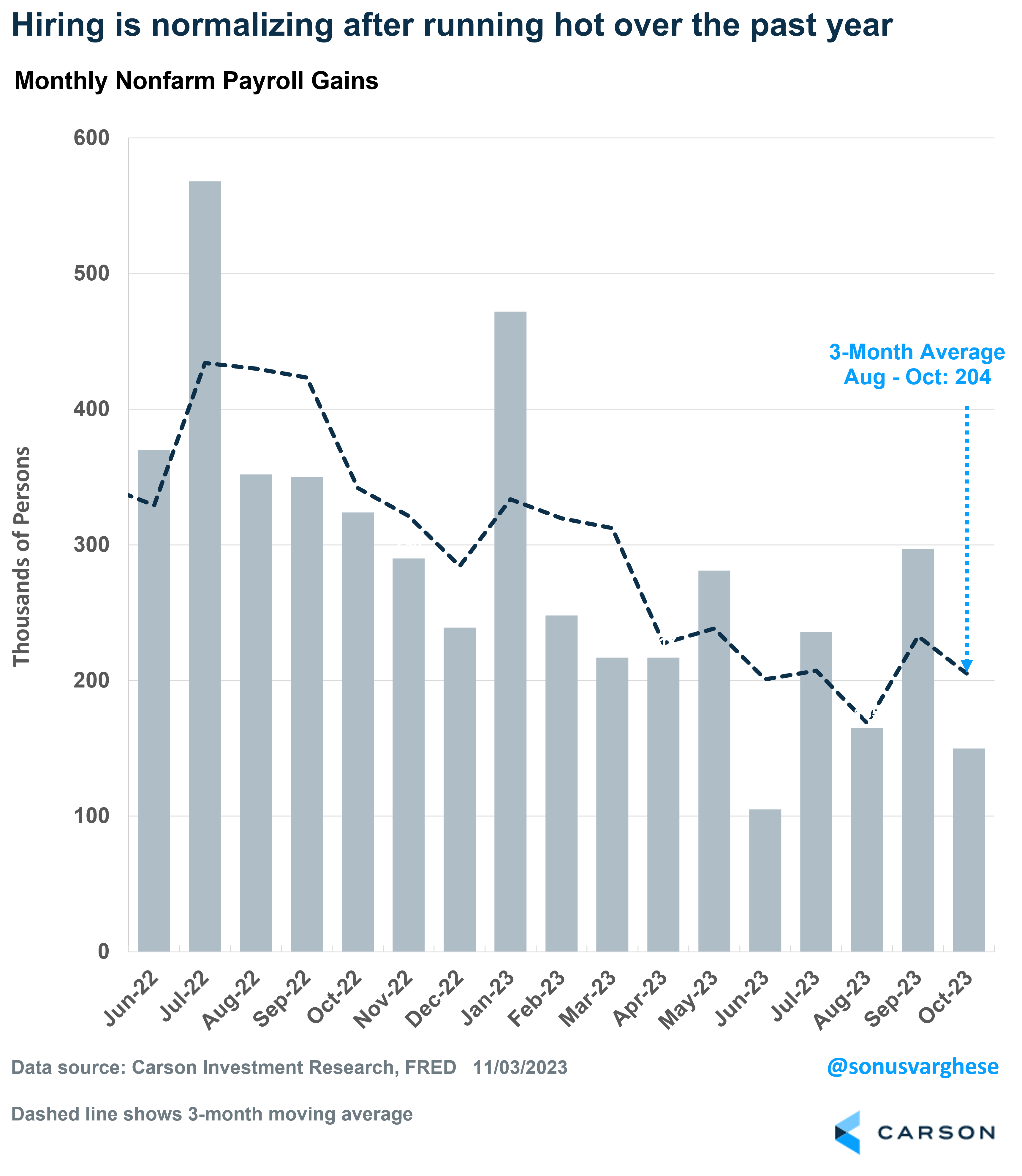

- Monthly job growth came in at 150,000, below expectations for a 180,000 gain.

- The unemployment rate ticked up from 3.8% to 3.9%

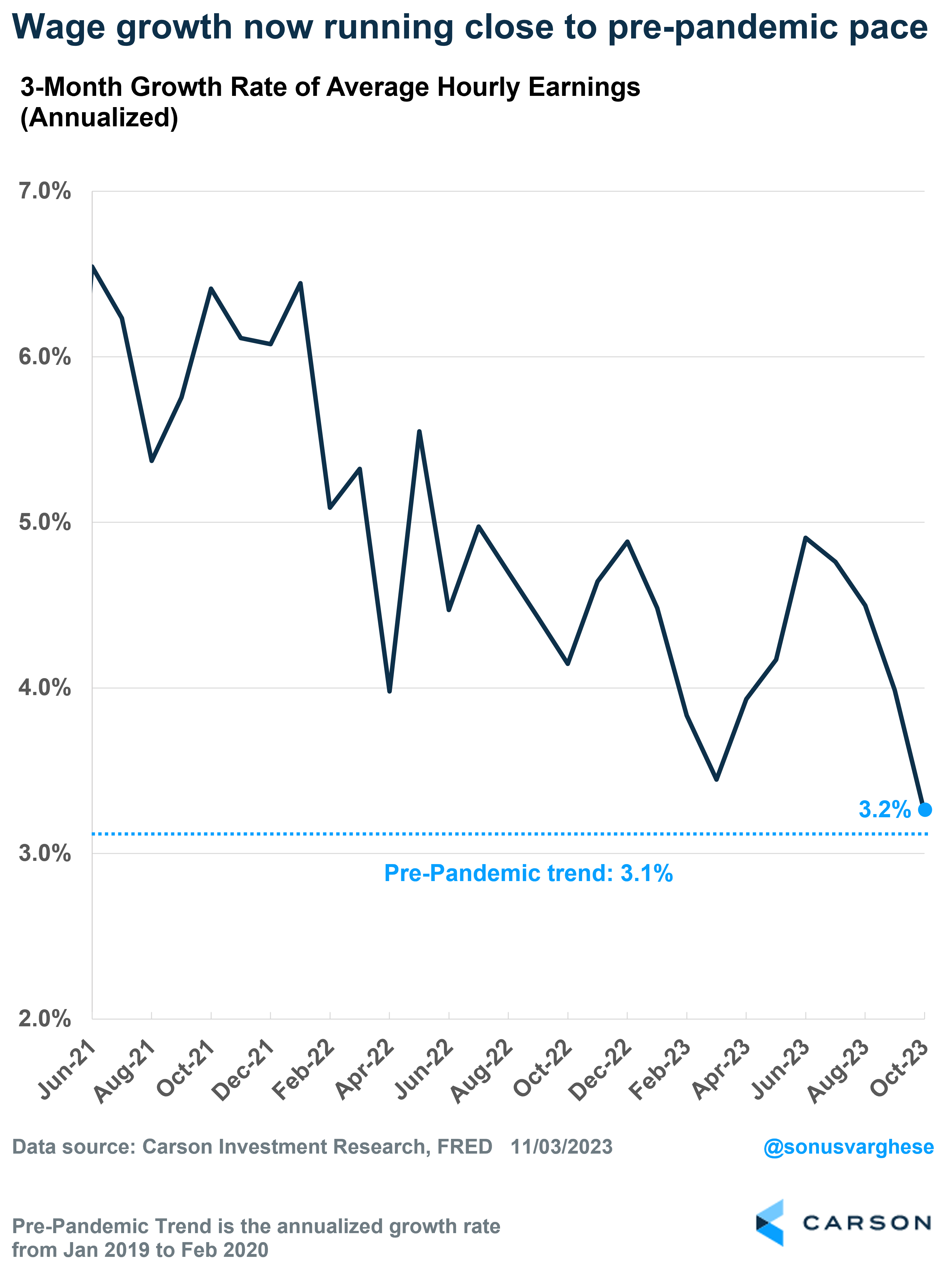

- Average hourly earnings growth rose at an annualized pace of 2.5% in October, well below expectations for close to a 4% increase.

But here’s some perspective on those numbers:

- Job growth was impacted by the United Auto Workers strike, which pulled manufacturing employment down by 33,000, and those are going to come back next month.

- Monthly job growth numbers can be noisy, and so the 3-month average is helpful to look at – that’s running at 204,000, which is above the 100,000 – 125,000 required to keep up with population growth.

- The unemployment rate doesn’t stay steady, nor does it keep going down in a straight-line during expansions. Between 1996 and 1999, the unemployment rate averaged 4.8%.

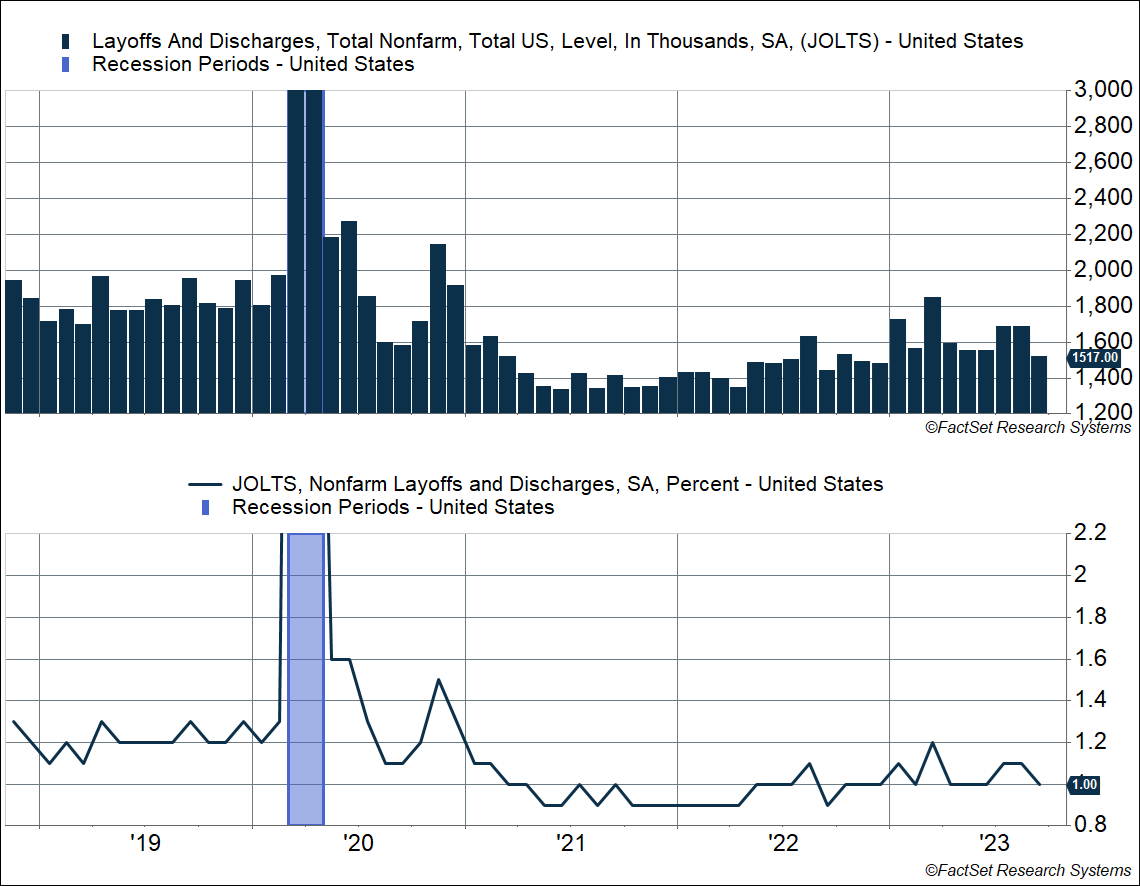

- A few days back the Bureau of Labor Statistics reported that layoffs are running around 1.5 million a month, which is well below the average 1.8 million in 2019.

- As a percent of employment, the layoff rate is now at 1% – before the pandemic, this averaged 1.2-1.3%. I’ve cut off the y-axis in the chart below to show what’s happening more clearly (layoffs surged in March-April 2020 during the pandemic).

The October payroll report tells us that the economy is slowing from its red-hot pace. However, we believe that’s just normalization rather than anything recessionary, for now.

But as the title of the blog says, this normalization is just what the doctor ordered for markets, and especially the Federal Reserve (Fed).

Good News: Fed Rate Hikes Are Probably Done

Here’s how markets reacted to the payroll report:

- Equity markets surged, rising more than 0.5% in the morning.

- The 10-year yield fell to 4.5% – it was around 5.0% 10 days ago.

- The probability of a Fed rate hike in December collapsed to under 10%, and the probability of one in January is now under 15%.

Safe to say, investors think the Fed is done with rate hikes, and they’re taking that as a big positive for equity markets. The 10-year yield had been rising for a few months now on the back of one strong economic data point after another, culminating in the Q3 GDP report which showed the economy growing at 4.9% last quarter. Things were bound to turn sooner rather than later – the economy certainly wasn’t going to grow anywhere close to that going forward. But we believe the underlying speed of the economy is close to trend, around 2.5%, versus falling into a sharp slowdown, or even a recession.

The Fed kept interest rates steady at 5.25-5.5% at their November meeting, pausing for the second meeting in a row. At their September meeting, members had penciled in one more rate hike for 2023. However, in his press conference, Fed Chair Powell brushed this away, saying the efficacy of those projections deteriorates within three months, and that Fed members could change their views at their December meeting.

Powell went on to say that risks are more balanced now, unlike last year. Last year the risk was that they wouldn’t do enough to curb inflation, and so they moved aggressively. However, right now, there’s also a risk of doing too much, and unnecessarily sending the economy into a recession. They believe that the cumulative impact of everything they’ve done so far is yet to impact the economy.

Moreover, if inflation continues to head lower, which is likely with wage growth cooling, we could see the Fed pivot to rate cuts by the middle of next year. Average hourly earnings are running at a 3.2% annualized pace over the past three months, almost matching what we saw pre-pandemic. That’s still strong, but something the Fed can live with.

If inflation looks to be on a sustainable path to their target of 2%, we could see them pivot sooner rather than later. By itself, keeping rates where they are when inflation is falling means policy is implicitly getting tighter. Powell doesn’t sound like someone who wants that. And if economic growth is at risk, they could act even more aggressively.

One thing we’ve seen with the Powell-led Fed is that they’ve been quick to pivot and act aggressively when they realize they’re behind the curve.

- In 2018-2019, financial stresses and a slowdown prompted an about-face and led them to eventually cut rates.

- In 2020 March, facing a deep recession, they didn’t hesitate to take rates to zero and took a series of aggressive measures to ease stresses in financial markets.

In 2022 June, facing a 40-year high in inflation, they pivoted to a much more aggressive pace of tightening. Looking ahead, what’s interesting is that a normalizing economy could result in looser financial conditions, which could boost cyclical activity. A lower 10-year interest rate will push mortgage rates lower and that could spur more activity in the housing market. Business investment will also likely rise.

Lower inflation will translate to consumers having more in their wallets as well, not to mention the fact that some household real estate wealth could be unlocked if there are refinancing opportunities. Think of someone who bought a mortgage at 8% but can now refinance at 6.5%. My colleague, Barry Gilbert, recently wrote about how there’s a lot of pent-up strength in the economy, despite all the pessimism.

Throw potentially easier monetary policy into the mix of an already resilient economy, and we may have a strong catalyst for equity markets to gear shift higher.

Ryan just wrote about how stocks pulled back in October, but November tends to be the best month of the year. Things may be falling into place here. Ryan and I also talked about all this in the latest episode of our Facts vs Feelings podcast. Take a listen below:

1967486-1123-A